Top Tips To Lower Your Vehicle Insurance Premiums

In today’s world, reducing your vehicle insurance premiums is more crucial than ever. By implementing some smart strategies, you can save money while still ensuring adequate coverage. In this article, we’ll explore the top tips to help you lower your insurance costs effectively.

⭐ Table of content

- Essential Strategies to Reduce Your Car Insurance Costs and Maximize Savings

- How to decrease car insurance premium?

- Which is the best strategy to reduce the cost of insurance premiums?

- What type of things can reduce a driver's insurance premium?

- What are 5 or more factors that increase your car insurance premiums?

Essential Strategies to Reduce Your Car Insurance Costs and Maximize Savings

When it comes to managing your finances, reducing car insurance costs can significantly enhance your budget. Here are some essential strategies to help you maximize savings on your car insurance premiums:

1. Shop Around for Quotes: Different insurers offer varying rates for similar coverage. Make sure to compare quotes from multiple providers to find the best deal.

2. Increase Your Deductible: Opting for a higher deductible can lower your premium. Just ensure you can afford the out-of-pocket expense in case of a claim.

⬇️ Look Also The Pros And Cons Of Comprehensive Vehicle Insurance

The Pros And Cons Of Comprehensive Vehicle Insurance3. Take Advantage of Discounts: Many insurers offer discounts for good driving records, safe vehicles, bundling policies, and low mileage. Be sure to ask about all available discounts.

4. Maintain a Good Credit Score: Insurers often use credit scores to determine premiums. Improving your credit score can lead to lower insurance rates.

5. Consider Usage-Based Insurance: If you drive less frequently or have a safe driving record, usage-based insurance could result in significant savings.

6. Review Your Coverage Regularly: As your needs change, so should your coverage. Review your policy annually to ensure you're not over-insured.

⬇️ Look Also What To Do After A Car Accident: A Guide To Filing A Claim

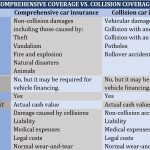

What To Do After A Car Accident: A Guide To Filing A Claim7. Drop Unnecessary Coverage: Evaluate whether certain coverages, like collision or comprehensive, are necessary based on the age and value of your vehicle.

8. Participate in a Defensive Driving Course: Completing a recognized defensive driving course can sometimes qualify you for discounts.

9. Keep Your Vehicle in Good Condition: Regular maintenance can prevent accidents and may qualify you for lower premiums due to lower risk.

10. Ask About Pay-as-You-Go Policies: These policies charge based on your actual driving habits, which could lead to savings if you drive infrequently.

⬇️ Look Also How Your Credit Score Impacts Vehicle Insurance Rates

How Your Credit Score Impacts Vehicle Insurance RatesBy implementing these strategies, you can effectively reduce your car insurance costs and improve your overall financial health.

Decreasing your car insurance premium can significantly impact your overall financial health. Here are some effective strategies to help you lower your car insurance costs:

1. Shop Around: Compare quotes from multiple insurance providers. This is essential since premiums can vary widely between companies. Use online comparison tools to make this process easier.

2. Increase Deductibles: By raising your deductible (the amount you pay out of pocket before insurance kicks in), you can lower your premium. Just ensure you can afford the higher deductible in case of an accident.

⬇️ Look Also How To Lower Your Home Insurance Costs Without Reducing Coverage

How To Lower Your Home Insurance Costs Without Reducing Coverage3. Maintain a Good Credit Score: Insurance companies often consider your credit score when determining premiums. A better credit score can lead to lower rates, so make sure to pay bills on time and reduce outstanding debts.

4. Take Advantage of Discounts: Many insurers offer a variety of discounts such as safe driver discounts, multi-car discounts, and bundling insurance policies. Always ask about available discounts that could apply to you.

5. Use a Telematics Program: Some insurance companies offer programs where you can save money by allowing them to track your driving habits. Safe driving can lead to significant discounts.

6. Limit Mileage: If you drive less than the average person, let your insurer know. Lower mileage often translates to lower risk, which can decrease your premium.

⬇️ Look Also A Beginner’s Guide To Vehicle Insurance For New Drivers

A Beginner’s Guide To Vehicle Insurance For New Drivers7. Choose the Right Car: The make and model of your vehicle can greatly affect your insurance rates. Typically, vehicles with higher safety ratings and lower theft rates tend to have lower premiums.

8. Review Your Coverage: Regularly reassess your coverage to ensure you’re not paying for unnecessary extras. For instance, if you have an older car, consider dropping collision or comprehensive coverage.

9. Complete Defensive Driving Courses: Some insurers provide discounts if you complete a defensive driving course, proving that you are a safer driver.

10. Stay Claims-Free: Avoiding claims can keep your premiums lower over time. Frequent claims can signal to insurers that you’re a higher-risk driver.

By implementing these strategies, you can effectively decrease your car insurance premium, leading to savings that can be allocated to other important financial goals. Remember to review your policy annually to reassess your needs and ensure you're still getting the best possible rate.

Reducing the cost of insurance premiums can be approached through several effective strategies. Here are some key methods:

1. Shop Around: Compare quotes from multiple insurance providers. This allows you to find the most competitive rates and better coverage options.

2. Increase Deductibles: Consider opting for a higher deductible. This usually lowers your premium, but it’s important to ensure that you can afford the out-of-pocket expense in case of a claim.

3. Bundle Policies: Many insurers offer discounts if you bundle multiple policies, such as home, auto, and life insurance. This can lead to significant savings.

4. Maintain a Good Credit Score: A higher credit score often translates to lower premiums. Insurers frequently use credit scores as a factor in determining rates, so maintaining good credit can help reduce costs.

5. Take Advantage of Discounts: Inquire about available discounts based on factors like safe driving records, completing defensive driving courses, or being claims-free for several years.

6. Review Coverage Needs: Regularly assess your insurance needs and adjust your coverage accordingly. Eliminating unnecessary coverage can lower your premiums.

7. Install Safety Devices: For car insurance, installing safety features or anti-theft devices can lead to discounts on your premiums. Similarly, home security systems can also lower home insurance costs.

8. Avoid Small Claims: Frequent claims can increase your premium. It may be more cost-effective to pay out-of-pocket for minor damages instead of filing a claim.

By implementing these strategies, you can effectively reduce your insurance premiums and potentially save a significant amount of money over time.

There are several factors that can help reduce a driver's insurance premium. Here are some key elements:

1. Safe Driving Record: Maintaining a clean driving history with no accidents or traffic violations can significantly decrease your premiums. Insurers often reward safe drivers with lower rates.

2. Bundling Policies: Purchasing multiple insurance policies (such as home and auto) from the same provider can lead to substantial discounts. This is known as bundling, and it can save you a good amount on your overall insurance costs.

3. Higher Deductibles: Choosing a higher deductible means you'll pay more out of pocket in the event of a claim, but it can lower your monthly premium. It's important to choose a deductible that you can afford in case of an incident.

4. Taking Defensive Driving Courses: Completing a defensive driving course can qualify you for a discount on your insurance. These courses not only enhance your driving skills but also show insurers that you are committed to safer driving.

5. Low Mileage Discounts: If you drive fewer miles than the average person, you may be eligible for discounts. Many insurance companies offer reduced rates for low mileage drivers, as less time on the road means a lower risk of accidents.

6. Good Credit Score: In many states, insurers consider your credit score when determining your premium. A better credit score typically leads to lower rates, as it is seen as an indicator of responsible behavior.

7. Installing Safety Features: Equipping your vehicle with advanced safety features like anti-lock brakes, airbags, and anti-theft devices can lead to discounts. Insurers may offer lower premiums for cars that have features designed to prevent accidents or theft.

8. Choosing the Right Vehicle: The make and model of your car can affect your premiums. Vehicles that are considered safer or have lower repair costs generally attract lower insurance rates.

9. Reviewing Coverage Options: Regularly reviewing and adjusting your coverage can help you identify unnecessary extras that you can eliminate. It's wise to assess your policy annually to ensure you're not over-insured.

10. Loyalty Discounts: Staying with the same insurance company for an extended period can earn you loyalty discounts. Many providers reward long-term customers with reduced rates.

By actively considering these factors, drivers can take steps to potentially lower their auto insurance premiums. Always remember to compare quotes from different insurers to find the best deal for your specific situation.

There are several factors that can significantly increase your car insurance premiums. Understanding these can help you manage and possibly reduce your insurance costs. Here are five key factors:

1. Driving Record: A history of accidents or traffic violations can lead to higher premiums. Insurers view you as a higher risk if you've been in multiple accidents or received tickets for speeding, reckless driving, or DUI offenses. A clean driving record typically results in lower premiums.

2. Location: The area where you live can greatly impact your insurance rates. Areas with high crime rates or heavy traffic may result in increased premiums. Urban environments often see higher rates compared to rural areas.

3. Type of Vehicle: The make and model of your car affect your insurance costs. High-end vehicles, sports cars, or those with high theft rates usually come with higher premiums. Insurance companies consider the cost of repairs and safety ratings.

4. Age and Gender: Younger drivers, especially males, tend to pay higher premiums due to their perceived higher risk. Insurance statistics often show that younger, less experienced drivers are more likely to be involved in accidents.

5. Credit Score: Many insurers use credit scores as a factor in determining premiums. A lower credit score may indicate higher risk, leading to elevated insurance costs. Maintaining good credit can help secure better rates.

6. Coverage Options: The level of coverage you choose, such as full coverage versus just liability, impacts your premiums. Higher coverage limits and additional options like roadside assistance can increase costs.

By considering these factors, you can take proactive steps to potentially lower your car insurance premiums.

What are the most effective strategies to reduce my vehicle insurance premiums?

To effectively reduce your vehicle insurance premiums, consider the following strategies:

1. Increase your deductible: Opting for a higher deductible can significantly lower your monthly premium.

2. Bundle policies: Combine your auto insurance with other policies like home or health insurance for discounts.

3. Maintain a good credit score: Insurers often use credit scores as a factor; a higher score can lead to better rates.

4. Take advantage of discounts: Look for discounts offered for safe driving, low mileage, or completing defensive driving courses.

5. Review coverage needs: Periodically reassess your policy to eliminate unnecessary coverage on older vehicles.

By implementing these methods, you can effectively lower your vehicle insurance costs.

How does my driving record impact my vehicle insurance rates?

Your driving record significantly impacts your vehicle insurance rates. Insurance companies assess risk based on your history; a clean record typically leads to lower premiums, while accidents or traffic violations can result in higher rates. Maintaining a good driving record is essential for cost-effective insurance.

Are there discounts available that I might be missing for my vehicle insurance?

Yes, there are often discounts available for vehicle insurance that you might be missing. Common discounts include those for safe driving records, multi-policy bundling, good student status, and low mileage. It's advisable to shop around and ask your insurer about any potential discounts applicable to your situation.

En este sentido, te presentamos un video que ofrece los mejores consejos para reducir las primas de seguro de tu vehículo.

How To Handle A Denied Vehicle Insurance Claim

The Benefits Of Usage-Based Vehicle Insurance Policies

Vehicle Insurance For Electric Cars: What You Need To Know

How Driving Habits Affect Vehicle Insurance Rates

The Importance Of Gap Insurance For New Car Owners

How To Compare Vehicle Insurance Quotes Effectively

Deja una respuesta