Top 5 Health Insurance Options For Self-Employed Individuals

In today's dynamic economy, self-employed individuals face unique challenges when it comes to healthcare. Choosing the right health insurance is essential for maintaining both financial and physical well-being. In this article, we explore the top 5 health insurance options tailored specifically for the self-employed.

⭐ Table of content

- Essential Guide to the Best Health Insurance Plans for Freelancers and Self-Employed Professionals

- What type of insurance should a self-employed person have?

- How do self-employed people afford health insurance?

- Can you write off health insurance if you are self-employed?

- Is 0 a month a lot for health insurance?

Essential Guide to the Best Health Insurance Plans for Freelancers and Self-Employed Professionals

When it comes to finding the best health insurance plans for freelancers and self-employed professionals, understanding your options is crucial. Freelancers often lack the benefits that come with traditional employment, making health insurance a top priority.

One of the first steps is to assess your healthcare needs. Consider factors such as your age, existing health conditions, and the frequency of doctor visits. These variables will help you determine whether you need a plan with lower deductibles or if a high-deductible health plan (HDHP) might be more cost-effective for you.

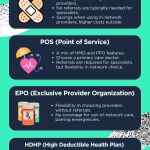

Next, evaluate different types of health insurance plans. Individual health insurance plans can offer tailored coverage, while Health Maintenance Organizations (HMOs) generally require you to choose a primary care physician and get referrals for specialists. On the other hand, Preferred Provider Organizations (PPOs) offer more flexibility in choosing healthcare providers but often come with higher premiums.

⬇️ Look Also How To Save Money On Health Insurance Without Sacrificing Coverage

How To Save Money On Health Insurance Without Sacrificing CoverageAnother alternative is a Health Savings Account (HSA), which allows you to save money tax-free for medical expenses if you have a qualifying HDHP. This can provide a valuable financial cushion for unexpected healthcare costs.

Consider the overall cost. Beyond premiums, evaluate out-of-pocket expenses like deductibles, co-pays, and coinsurance. It’s essential to factor in these costs when selecting a plan, as they can significantly affect your financial situation.

Finally, look into government programs like the Affordable Care Act (ACA). Through the ACA marketplace, freelancers may qualify for subsidies based on their income, making health insurance more affordable. Always review the terms and conditions thoroughly to avoid any unexpected charges or limitations.

Choosing the right health insurance plan is vital for protecting your health and financial stability as a freelancer or self-employed individual. By carefully considering your options and understanding the nuances of each plan, you can make an informed decision that best suits your lifestyle and budget.

⬇️ Look Also Health Insurance For Expats: What You Need To Know

Health Insurance For Expats: What You Need To KnowWhat type of insurance should a self-employed person have?

For a self-employed person, having the right insurance coverage is crucial to protect against unexpected events that could impact both personal and business finances. Here are some types of insurance that a self-employed individual should consider:

1. Health Insurance: It's essential to have health insurance to cover medical expenses. This can prevent significant financial strain in case of illness or injury.

2. Liability Insurance: Depending on the nature of the work, professional liability insurance (also known as errors and omissions insurance) protects against claims of negligence or inadequate work. Additionally, general liability insurance safeguards against third-party claims for bodily injury or property damage.

3. Disability Insurance: This type of insurance provides income replacement if you become unable to work due to illness or injury. It’s vital for self-employed individuals who do not have employee benefits.

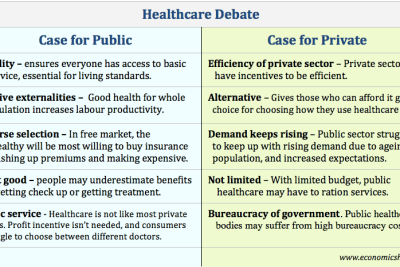

⬇️ Look Also The Pros And Cons Of Private Vs. Public Health Insurance

The Pros And Cons Of Private Vs. Public Health Insurance4. Property Insurance: If you have a home office or physical business location, property insurance can help cover the cost of repairs or replacements due to theft, fire, or other damages.

5. Business Interruption Insurance: This coverage can help compensate for lost income and operating expenses if your business is temporarily unable to operate due to a covered event.

6. Life Insurance: For those with dependents, life insurance ensures that your family is financially secure in the event of your untimely death.

7. Auto Insurance: If you use your vehicle for business purposes, it’s crucial to have commercial auto insurance to cover potential accidents or liabilities.

⬇️ Look Also The Impact Of Health Insurance On Mental Health Care Access

The Impact Of Health Insurance On Mental Health Care Access8. Cyber Liability Insurance: If your business involves storing sensitive data or operating online, cyber liability insurance can protect against data breaches and cyber attacks.

In summary, self-employed individuals should carefully assess their risks and ensure they have adequate coverage in place to protect their health, income, and business assets. This proactive approach can help secure their financial future.

How do self-employed people afford health insurance?

Self-employed individuals often face unique challenges when it comes to affording health insurance. Here are some key strategies they use to manage this important expense:

1. Marketplace Insurance Plans: Many self-employed people turn to the Health Insurance Marketplace, where they can compare various plans and potentially qualify for subsidies based on their income. This can significantly lower their monthly premiums.

⬇️ Look Also Wells Fargo 500 Credit Score Home Loan

Wells Fargo 500 Credit Score Home Loan2. Deductible Expenses: Health insurance premiums for self-employed individuals can be deducted as a business expense on their taxes. This deduction can reduce taxable income, making insurance more affordable. It's crucial to keep thorough records of these expenses.

3. Health Savings Accounts (HSAs): Some opt for high-deductible health plans (HDHPs), which allow them to contribute to Health Savings Accounts. These accounts offer tax advantages and can help cover out-of-pocket medical expenses.

4. COBRA Coverage: For those transitioning from an employer-sponsored plan, COBRA allows them to continue their previous health insurance for a limited time. However, they will pay the full premium, which can be costly.

5. Professional Associations: Joining a professional association can provide access to group health insurance plans, which may offer lower rates compared to individual plans.

6. Negotiating Medical Bills: Self-employed individuals often need to be proactive in negotiating medical bills or seeking out healthcare providers that offer sliding scale fees based on income, thereby managing costs more effectively.

7. Budgeting for Health Insurance: Finally, it's essential for self-employed individuals to include health insurance premiums in their financial planning and budget accordingly. Setting aside a portion of profits specifically for health coverage can alleviate financial stress.

By exploring these options, self-employed people can find ways to afford health insurance while managing their overall financial health.

Can you write off health insurance if you are self-employed?

Yes, if you are self-employed, you can generally write off health insurance premiums as a business expense on your taxes. Here are some key points to consider:

1. Eligibility: To qualify for the deduction, you must be self-employed and report your income on Schedule C of your tax return. This applies whether you're a sole proprietor, a partner in a partnership, or a shareholder in an S corporation.

2. Deduction Limits: You can deduct 100% of your health insurance premiums paid for yourself, your spouse, and your dependents. This includes premiums for medical, dental, and long-term care insurance.

3. Income Considerations: The deduction cannot exceed your net earnings from self-employment. If your net earnings are low, it could limit the amount you can deduct.

4. Claiming the Deduction: To claim this deduction, use Form 1040 and report it on the Adjusted Gross Income (AGI) section. It is an "above-the-line" deduction, meaning you can take it even if you do not itemize deductions.

5. Other Types of Insurance: Additionally, if you pay for premiums for a spouse or dependents, you need to ensure those premiums are also eligible under the same rules.

6. Health Savings Accounts (HSAs): If you have an HSA, you can contribute to that account and deduct those contributions as well, further reducing your taxable income.

In summary, self-employed individuals can write off health insurance premiums as a business expense, which can significantly impact their overall tax liability. Always consult with a tax professional to ensure you meet all requirements and maximize your deductions.

Is $200 a month a lot for health insurance?

Whether $200 a month is a lot for health insurance can depend on several factors:

1. Location: Health insurance costs can vary significantly based on where you live. In some states or regions, $200 may be considered low, while in others, it could be high.

2. Coverage Level: The amount of coverage provided plays a crucial role. If the plan includes comprehensive benefits, lower deductibles, and lower co-pays, $200 might be a good deal. Conversely, if it offers minimal coverage, it could be more expensive than necessary.

3. Age and Health Status: Young, healthy individuals often have lower premiums compared to older adults or those with pre-existing conditions. Therefore, for a young and healthy person, $200 might seem high, but for an older individual, it could be reasonable.

4. Type of Plan: Employer-sponsored plans may have different rates than individual plans. Group plans typically offer lower rates due to shared risk among many participants.

5. Government Subsidies: If you're eligible for subsidies through platforms like the Affordable Care Act (ACA), your effective cost may be lower than $200, making it relatively affordable in the context of your overall financial situation.

In summary, whether $200 a month is a lot for health insurance depends on your specific situation, including location, coverage level, age, and health needs. It’s essential to compare different plans and consider what best meets your health and financial needs.

What are the top health insurance options available for self-employed individuals?

Self-employed individuals have several health insurance options to consider:

1. Marketplace Plans: Affordable Care Act (ACA) plans offer a range of coverage levels and potential subsidies based on income.

2. Health Savings Account (HSA): Coupled with a high-deductible plan, HSAs provide tax advantages for medical expenses.

3. Short-Term Health Insurance: Temporary plans that are generally lower-cost but offer limited coverage and benefits.

4. Professional Associations: Some trade groups provide access to group health plans, which can be more affordable than individual plans.

5. COBRA: If you recently left a job, you might be eligible to continue your previous employer's coverage through COBRA.

Exploring these options can help self-employed individuals find the right balance between cost and coverage.

How can self-employed individuals determine the best health insurance plan for their needs?

Self-employed individuals can determine the best health insurance plan for their needs by following these steps:

1. Assess Health Needs: Evaluate current health conditions and expected medical expenses.

2. Budgeting: Determine how much can be spent on premiums without compromising financial stability.

3. Research Plans: Compare different plans by considering factors like coverage options, deductibles, and out-of-pocket costs.

4. Check Networks: Ensure preferred doctors and hospitals are in the plan's network to avoid additional costs.

5. Consider Subsidies: Investigate eligibility for government subsidies under the Affordable Care Act, which can lower premium costs.

By focusing on these key areas, self-employed individuals can make an informed decision that aligns with their financial situation and health requirements.

What are the financial implications of choosing a specific health insurance option for self-employed individuals?

Choosing a specific health insurance option for self-employed individuals has significant financial implications. It can affect monthly premiums, deductibles, and <strong$out-of-pocket expenses, impacting overall cash flow. Higher premiums may provide better coverage but could strain budgets, while lower-cost plans might lead to higher costs in case of unexpected health issues. Additionally, the choice may affect tax deductions, as some plans can qualify for tax breaks. Ultimately, careful evaluation is crucial to align health needs with financial stability.

Para ayudarte a tomar decisiones informadas, a continuación, te presentamos un video que explora las cinco mejores opciones de seguros de salud para personas autoempleadas.

The Impact Of Health Insurance On Mental Health Care Access

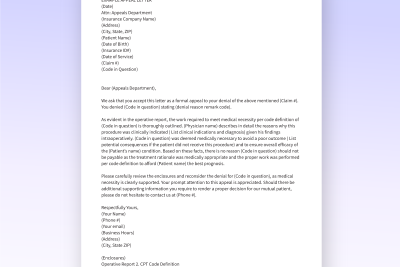

How To Appeal A Denied Health Insurance Claim

5 Common Myths About Health Insurance Debunked

How And When To Enroll In Health Insurance

The Pros And Cons Of Private Vs. Public Health Insurance

Health Insurance For Expats: What You Need To Know

Deja una respuesta