5 Common Myths About Health Insurance Debunked

In today's world, understanding health insurance is crucial. Many people hold misconceptions that can lead to poor decisions. In this article, we will debunk five common myths about health insurance, providing clarity and empowering you to make informed choices for your health and finances.

⭐ Table of content

Dispelling 5 Misconceptions About Health Insurance That Could Impact Your Financial Well-Being

Understanding health insurance is crucial for your financial well-being. Here are five misconceptions that you need to unravel:

1. Health insurance covers all medical expenses. Many believe that having health insurance means all their medical costs will be fully covered. In reality, most plans include deductibles, copayments, and out-of-pocket limits that can lead to significant expenses. It's important to read the fine print of your policy to understand what is and isn’t covered.

2. Higher premiums mean better coverage. While it might seem that paying higher premiums guarantees more comprehensive coverage, this isn't always true. Different plans may vary widely in terms of benefits, networks, and limitations. A plan with lower premiums could offer more cost-effective solutions for your specific health needs.

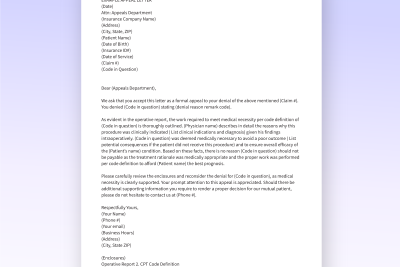

⬇️ Look Also How To Appeal A Denied Health Insurance Claim

How To Appeal A Denied Health Insurance Claim3. You only need health insurance when you're sick. This misconception can have severe financial consequences. Medical emergencies can arise unexpectedly, and lacking coverage at such times can lead to crippling medical bills. Maintaining continuous health insurance helps protect you from unforeseen financial strain.

4. All health insurance plans are the same. Not all health insurance policies offer the same terms or benefits. Understanding the differences between various types of plans, such as HMOs, PPOs, and EPOs, can greatly influence your healthcare experience and financial implications. Each has its own network of providers and rules regarding referrals and out-of-network care.

5. Employer-sponsored health insurance is always the best option. While employer plans can be advantageous, they may not be the most suitable choice for everyone. Individual plans might offer better coverage or lower costs based on personal health conditions and financial situations. It's essential to compare and evaluate all available options instead of defaulting to an employer's offering.

These misconceptions can significantly impact your financial decisions related to healthcare. Educating yourself about the nuances of health insurance is vital for making informed choices that align with your financial goals.

⬇️ Look Also The Impact Of Health Insurance On Mental Health Care Access

The Impact Of Health Insurance On Mental Health Care AccessWhat are the top 5 worst health insurance companies?

When evaluating health insurance companies, there are several factors to consider, including customer satisfaction, claim denial rates, coverage options, and overall financial stability. While opinions may vary, some health insurance companies are frequently mentioned in discussions about poor performance. Here are five companies that have often received negative attention:

1. UnitedHealthcare: This company has faced criticism for its high claim denial rates and a lack of transparency in policy details. Customers often report difficulties with obtaining approvals for necessary treatments.

2. Anthem Blue Cross Blue Shield: Known for inconsistent customer service, Anthem has been criticized for complex billing practices and long wait times for claims processing, which can frustrate policyholders.

3. Cigna: Although Cigna offers a range of plans, it has come under fire for poor network coverage in some areas and frequent claim denials for pre-existing conditions, making it challenging for members to access required care.

⬇️ Look Also 10 Key Questions To Ask Before Choosing A Health Insurance Plan

10 Key Questions To Ask Before Choosing A Health Insurance Plan4. Aetna: Aetna has faced complaints regarding the quality of customer service and issues with processing claims in a timely manner. Users have reported unexpected out-of-pocket costs due to unclear policy information.

5. Humana: Despite offering Medicare Advantage plans, Humana has received negative feedback about its limited provider network and inadequate responses to customer service inquiries, leading to dissatisfaction among users.

It's important to conduct thorough research and consider your personal healthcare needs when choosing a health insurance provider. Checking reviews, examining financial ratings, and consulting with professionals can lead to better decisions in the realm of health insurance.

What is a con of having a health insurance policy?

One significant con of having a health insurance policy is the cost of premiums. Health insurance can be expensive, and policyholders often have to pay monthly premiums that can strain their budgets. Additionally, there are often deductibles and co-pays that must be met before coverage kicks in, which can lead to unexpected out-of-pocket expenses. This means that even with insurance, individuals may still face substantial costs for medical care, which can impact their overall financial stability. Furthermore, some policies may have limitations and exclusions, meaning certain treatments or services may not be covered, potentially leading to additional financial burden when unexpected health issues arise.

⬇️ Look Also A Beginner's Guide To Understanding Health Insurance Terms

A Beginner's Guide To Understanding Health Insurance TermsWhat are the 5 factors of health insurance?

When considering health insurance in the context of finance, several key factors play a crucial role. Here are five significant factors:

1. Premiums: The monthly payment made to maintain the health insurance policy. Higher premiums often correlate with more extensive coverage and lower out-of-pocket costs.

2. Deductibles: This is the amount that the insured must pay out-of-pocket before the insurance company starts to pay for covered services. A higher deductible typically means lower premiums but can lead to higher costs in case of medical needs.

3. Co-payments and Coinsurance: These are shared costs between the insured and the insurer after the deductible is met. Co-payments are fixed amounts, while coinsurance is a percentage of the total cost of a service.

4. Network of Providers: Health plans often have a network of doctors and hospitals that they partner with. Staying within this network usually results in lower costs; going outside it can lead to higher expenses or no coverage at all.

5. Out-of-Pocket Maximum: This is the most an individual will have to pay for covered services in a policy period. Once this limit is reached, the insurance pays 100% of the costs for covered services, providing financial protection against catastrophic health events.

Understanding these factors can significantly impact your financial planning and decision-making when selecting a health insurance policy.

What is a false claim in health insurance?

A false claim in health insurance refers to the submission of inaccurate or misleading information in order to obtain benefits or payment from an insurance provider. This can occur in various ways, including:

1. Fabricating medical services: Claiming that a treatment or procedure was performed when it did not actually take place.

2. Exaggerating costs: Inflating the cost of medical services to receive a higher reimbursement than what is justified.

3. Misrepresenting the patient’s condition: Providing false information about a patient’s diagnosis or treatment needs to secure coverage for an unnecessary procedure.

The consequences of filing a false claim can be severe, including financial penalties, loss of insurance coverage, and even criminal charges. Insurers often have robust systems in place to detect such fraudulent activities, as they significantly impact healthcare costs and the overall integrity of the insurance system. Thus, maintaining honesty and accuracy in health insurance claims is crucial for both providers and patients to ensure a fair and sustainable healthcare environment.

What are the financial implications of believing common myths about health insurance?

Believing common myths about health insurance can lead to significant financial repercussions. For example, assuming that all plans cover the same services may result in unexpected out-of-pocket costs if needed care isn’t covered. Additionally, underestimating premiums or ignoring the benefits of preventive care can lead to higher overall healthcare expenses. Misconceptions can also cause individuals to forgo necessary coverage, leading to financial strain from medical emergencies. In summary, staying informed and understanding your plan is crucial to avoid unnecessary expenses and ensure adequate protection.

How can understanding health insurance myths help with budgeting for healthcare expenses?

Understanding health insurance myths can greatly enhance your ability to budget for healthcare expenses. By debunking common misconceptions, you can make more informed choices about your insurance plan, leading to better coverage and lower out-of-pocket costs. This knowledge helps in identifying hidden fees and discounts, allowing for a more accurate forecast of annual healthcare spending. Ultimately, addressing these myths fosters financial preparedness and reduces the risk of unexpected medical bills.

What are the long-term financial effects of choosing a health plan based on misconceptions?

Choosing a health plan based on misconceptions can lead to significant long-term financial strain. Individuals may incur unexpected medical costs due to inadequate coverage or high out-of-pocket expenses. Moreover, poor choices can result in higher premiums over time as individuals may face penalties or need to switch plans later. Ultimately, this choice can affect their overall financial stability and savings potential in the long run.

Para aclarar cualquier confusión sobre el tema, a continuación te presentamos un video que desmantela cinco mitos comunes sobre el seguro de salud.

The Impact Of Health Insurance On Mental Health Care Access

How To Appeal A Denied Health Insurance Claim

How And When To Enroll In Health Insurance

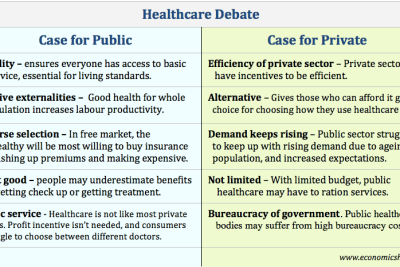

The Pros And Cons Of Private Vs. Public Health Insurance

Health Insurance For Expats: What You Need To Know

How To Save Money On Health Insurance Without Sacrificing Coverage

Deja una respuesta