How To Fix Credit Score

Improving your credit score is essential for achieving financial stability. In this article, we will discuss effective strategies to enhance your credit rating, enabling you to secure better loans and interest rates. Let's dive into the steps you can take to fix your credit score!

⭐ Table of content

Essential Steps to Improve Your Credit Score: A Comprehensive Guide

Understanding your credit score is crucial for making informed financial decisions. Your credit score is a three-digit number that lenders use to assess the risk of lending you money. The higher your score, the less risk you pose to lenders.

Check your credit report regularly. You are entitled to one free credit report per year from each of the three major credit bureaus: Experian, TransUnion, and Equifax. Reviewing your credit report helps you identify any errors or inaccuracies that may negatively impact your score.

Pay your bills on time. Payment history accounts for a significant portion of your credit score. Setting up automatic payments or reminders can help ensure that you never miss a due date.

⬇️ Look Also What Is The Highest Credit Score Possible

What Is The Highest Credit Score PossibleReduce your credit utilization ratio. Keep your credit card balances low relative to your credit limits. A good rule of thumb is to maintain a utilization ratio below 30%. This shows lenders that you are responsible with credit.

Avoid opening too many new accounts at once. Each time you apply for credit, a hard inquiry is made on your report, which can temporarily lower your score. Opening several new accounts in a short period can signal financial distress to lenders.

Establish a long credit history. The length of your credit history also contributes to your score. Keep older accounts open even if you don’t use them frequently, as they help to build a more established credit profile.

Diversify your credit mix. Having a varied mix of credit types—such as revolving credit (credit cards) and installment loans (car loans, mortgages)—can have a positive impact on your score. However, only take on credit that you need and can manage responsibly.

⬇️ Look Also Wells Fargo 500 Credit Score Home Loan

Wells Fargo 500 Credit Score Home LoanConsider becoming an authorized user. If you have a family member or friend with a good credit history, consider asking if they will add you as an authorized user on their credit card. This can help improve your credit score by leveraging their positive payment history.

Be patient and consistent. Improving your credit score takes time and consistent effort. Focus on implementing these steps diligently, and over time, you will likely see a positive change in your credit score.

How do I quickly fix my credit score?

Improving your credit score quickly can be challenging, but here are some effective steps you can take:

1. Check Your Credit Report: Obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Look for any errors or inaccuracies that could be negatively impacting your score.

⬇️ Look Also Credit Score Needed For American Express

Credit Score Needed For American Express2. Dispute Errors: If you find mistakes on your report, dispute them immediately. Correcting errors can lead to a quick boost in your credit score.

3. Pay Bills on Time: Your payment history is a significant factor in your credit score. Ensure that all your current bills are paid on time to avoid further damage to your score.

4. Reduce Credit Utilization: Aim to keep your credit utilization ratio below 30%. Pay down existing credit card balances or request a credit limit increase to improve your utilization ratio.

5. Avoid New Hard Inquiries: While it may be tempting to apply for new credit to improve your score, each application can result in a hard inquiry, which can temporarily lower your score. Limit new credit applications during this period.

⬇️ Look Also How To Improve Credit Score

How To Improve Credit Score6. Become an Authorized User: If you have a family member or friend with a good credit history, ask if they would add you as an authorized user on their credit card. This can help improve your credit score by benefiting from their positive credit behavior.

7. Consider a Secured Credit Card: If you are having trouble getting approved for traditional credit, consider applying for a secured credit card. Use it responsibly to build your credit history.

8. Stay Consistent: Continuously monitor your credit behavior. Maintain good habits like timely payments and low balances to gradually improve your score over time.

By following these steps diligently, you may see an improvement in your credit score in no time!

⬇️ Look Also How To Build Credit Score

How To Build Credit ScoreHow to get a 720 credit score in 6 months?

Achieving a 720 credit score in 6 months is ambitious, but with dedication and strategic actions, it can be attainable. Here’s a step-by-step guide:

1. Check Your Credit Report: Obtain your credit report from all three major credit bureaus—Equifax, Experian, and TransUnion—using AnnualCreditReport.com. Review it for any inaccuracies or errors that could negatively impact your score.

2. Dispute Errors: If you find any discrepancies, file disputes with the credit bureaus. Correcting errors can significantly improve your credit score.

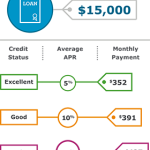

3. Pay Bills on Time: Ensure that all your payments—including credit cards, loans, and utilities—are made on or before their due date. Payment history is one of the most critical factors in your credit score, contributing to about 35% of the total score.

⬇️ Look Also What Credit Score Do You Start With

What Credit Score Do You Start With4. Reduce Credit Card Balances: Aim to keep your credit utilization ratio below 30%. This means if you have a credit limit of $10,000, try to keep your total outstanding balances under $3,000. Pay down existing balances and avoid accumulating new debt.

5. Avoid Opening New Accounts: Each time you apply for credit, a hard inquiry is recorded. Too many inquiries can lower your score. Instead, focus on managing your existing accounts.

6. Maintain Older Credit Accounts: The length of your credit history accounts for roughly 15% of your score. Keep older accounts open and in good standing, as they help strengthen your credit profile.

7. Consider Becoming an Authorized User: If you have a family member or close friend with a strong credit history, ask if you can become an authorized user on their account. This can help you benefit from their positive payment history.

8. Diversify Your Credit Types: Having a mix of credit (credit cards, installment loans, etc.) can positively impact your score. However, only take on new debt responsibly and when necessary.

9. Regularly Monitor Your Score: Use free credit monitoring tools to keep track of your progress. This will help you understand how your actions are affecting your score and allow you to adjust your strategy accordingly.

10. Stay Disciplined: Consistency is key. Stick to your plan, avoid unnecessary spending, and make every effort to adhere to deadlines.

By following these steps diligently, you increase your chances of reaching a 720 credit score within six months. Remember, patience and persistence are vital in the journey to improving your credit health.

Is it true that after 7 years your credit is clear?

In the context of finance, it's commonly believed that negative items on your credit report typically fall off after 7 years. This includes late payments, collections, and bankruptcies. However, there are some important points to consider:

1. Not all negative information lasts for the same duration. For instance, bankruptcies can remain on your credit report for 7 to 10 years, depending on the type of bankruptcy filed.

2. The 7-year rule applies primarily to consumer debt. Other types of financial data, like inquiries or settled debts, may have different timelines for removal from your report.

3. Your credit score may still be affected even after negative items fall off. If you’ve had significant credit issues in the past, rebuilding your credit will take time and positive credit behavior.

4. Credit reporting agencies are required to remove negative information after the specified time period, but it’s wise to check your credit report periodically to ensure accuracy.

In summary, while negative items typically clear from your credit report after 7 years, understanding the specifics and maintaining good credit practices is crucial for a healthy credit score.

How to raise your credit score 200 points in 30 days?

Raising your credit score by 200 points in just 30 days is a challenging task, but it can be achievable with dedication and the right strategies. Here are some steps you can take to improve your credit score significantly:

1. Check Your Credit Report

Obtain a free copy of your credit report from all three major bureaus: Experian, TransUnion, and Equifax. Review it for any errors, such as incorrect account information or late payments. Dispute any inaccuracies you find, as correcting these can positively impact your score.

2. Pay Off Outstanding Debts

Focus on paying down existing debts, particularly on credit cards. Aim to reduce your credit utilization ratio (the amount of credit used versus the total credit limit) to below 30%. If possible, pay off debts entirely to maximize your score.

3. Make All Payments on Time

Ensure that you make all of your payments on time, including credit cards, loans, and other bills. Set up automatic payments or reminders to avoid late fees, as timely payments are crucial for building a positive credit history.

4. Increase Your Credit Limit

Contact your credit card issuers to request a credit limit increase. This can help lower your credit utilization ratio, as long as you do not increase your spending. A higher credit limit allows for better utilization percentages.

5. Avoid New Hard Inquiries

While you may be tempted to open new credit accounts to improve your score, doing so can result in hard inquiries that temporarily lower your credit score. Instead, focus on maintaining your existing accounts.

6. Become an Authorized User

Consider becoming an authorized user on a family member’s or friend’s credit card with a good payment history. This can add their positive credit history to your report, potentially boosting your score without the responsibility of the debt.

7. Use a Credit-Builder Loan

If available, consider taking out a credit-builder loan. These loans are designed to help individuals improve their credit scores by reporting timely payments to the credit bureaus.

8. Monitor Your Progress

Use credit monitoring tools to keep track of your credit score. This will help you understand the impact of your actions and motivate you to continue improving your credit habits.

By following these steps diligently, you can potentially raise your credit score significantly. Remember, while achieving a 200-point increase in 30 days is ambitious, consistent effort will lead to improvement over time. Stay committed to making sound financial decisions!

What are the effective steps to improve my credit score?

To improve your credit score, follow these effective steps:

1. Pay your bills on time to establish a positive payment history.

2. Reduce your credit card balances to lower your credit utilization ratio.

3. Avoid opening new credit accounts unnecessarily, as this can impact your average account age.

4. Check your credit report regularly for errors and dispute any inaccuracies.

5. Keep old credit accounts open, as they contribute to the length of your credit history.

By focusing on these key areas, you can significantly boost your credit score over time.

How long does it take to see improvements in my credit score after making changes?

The time it takes to see improvements in your credit score after making changes can vary, but typically you may notice changes within 3 to 6 months. Consistently managing credit responsibly, such as paying bills on time and reducing debt, will gradually reflect in your score. Remember, patience is key as credit scores are calculated based on long-term behavior.

Are there specific strategies to dispute inaccuracies on my credit report to boost my score?

Yes, there are specific strategies to dispute inaccuracies on your credit report to boost your score. First, obtain a copy of your credit report from all three major bureaus. Next, identify errors such as incorrect account information or outdated details. Then, file a dispute with the credit bureau online or via mail, providing supporting documentation to back up your claims. Finally, follow up to ensure that the inaccuracies are corrected and monitor your score for changes.

En este sentido, te invitamos a ver el siguiente video que te guiará sobre cómo arreglar tu puntaje crediticio de manera efectiva.

What Licenses Are Needed To Start A Cleaning Business

Credit Score Needed For Discover Card

Minimum Credit Score To Lease A Car

Credit Score Simulator Credit Karma

Credit Score Needed For Apple Card

Credit Score For Amazon Card

Deja una respuesta